|

September 27, 2008

The prospect of Congress reaching swift agreement on the Bush Administration's $US700 billion fund to stabilise the world's financial markets has deteriorated sharply, despite the collapse of Washington Mutual, the biggest bank to fold in US history and banks having all but stopped lending to each.

Ironically it is the House Republicans rebelling, despite the recent history of Republicans attempting to undermine the constitutional checks and balances by removing judicial reviews legislatively, or supporting the executive branch doing so., in order to establish executive dominance over Congress.

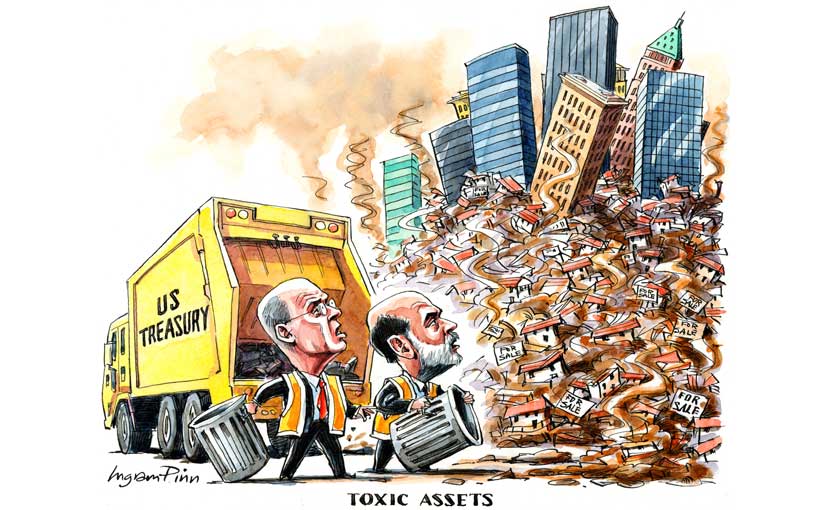

Ingram Penn, toxic assets, 2008

Ingram Penn, toxic assets, 2008

Investment banking’s long boom is over and lean years lie ahead. The business is likely to be narrower in scope, subject to greater regulation, smaller and less profitable.

As Peter Thal Larsen and Francesco Guerrera go on to remind us:

it can be easy to forget that the industry was not always this large. As recently as the mid-1980s, most Wall Street firms were private partnerships, with limited capital, that specialised mainly in underwriting equity and bond offerings and providing advice to companies.Since then, fuelled by deregulation, consolidation and the globalisation of capital flows, they have transformed themselves into publicly traded behemoths, intermediating in a bewildering array of financial risks and placing huge bets with their own capital.

Leverage turbocharged profits by enabling banks to reap high returns from relatively small amounts of capital. Goldman and Morgan Stanley are the last examples of investment banks.The others have been subsumed into larger universal banks, which have a more diverse funding base, including retail deposits.

|

Here in Australia, we have property bubble to contend with. On the ABC news the other night, Alan Kohler presented a chart comparing US, UK and Australian residential property prices over the past 20 years. The prices of all three pretty much moved up in lock step. The housing bubble in the US has bust, and in the UK it's in the process of busting. This article titled "Don't put your house on it" discusses whether the Australian property market will follow the US and UK down.

http://www.the-diplomat.com/article.aspx?aeid=8724

The commodities boom may have given Australia a reprive, however I think prices are likely to decline for the following reasons.

1. There has been a lot of speculative activity propelling the boom. With rental property returning yeilds of only 1-2% most investers were seeking a capital gain. At the peak, 55% of all sales were attributable to investment capital, with first home buyers accounting for only 8%.

2. The boom has propelled prices way above their historical levels.

3. The boom was propelled by easy credit and not rising income levels, particularly in mortage land (outer suburbs of the major capital cities).

4. Risk that speculative capital may exit the market due to de-leveraging.

This article discusses de-leveraging.

http://www.creditwritedowns.com/2008/06/de-leveraging.html

Last week treasurer Swan announced that the Fed Govt would be injecting $4 billion into the residential propery credit markets under the guise of creating more competition. Is the Govt trying to counter the effects of credit contraction? How much tax payers money will it use trying to hold up prices? Credit contraction leads to asset price declines as there is less money to bid up prices. Currently the median house price in Sydney is $570,000, over 10 times average income.